The cost of Brexit: December 2021

By December 2021, leaving the single market and customs union had reduced UK goods trade by 14.9 per cent. And new analysis shows that UK exports have taken a larger hit than imports.

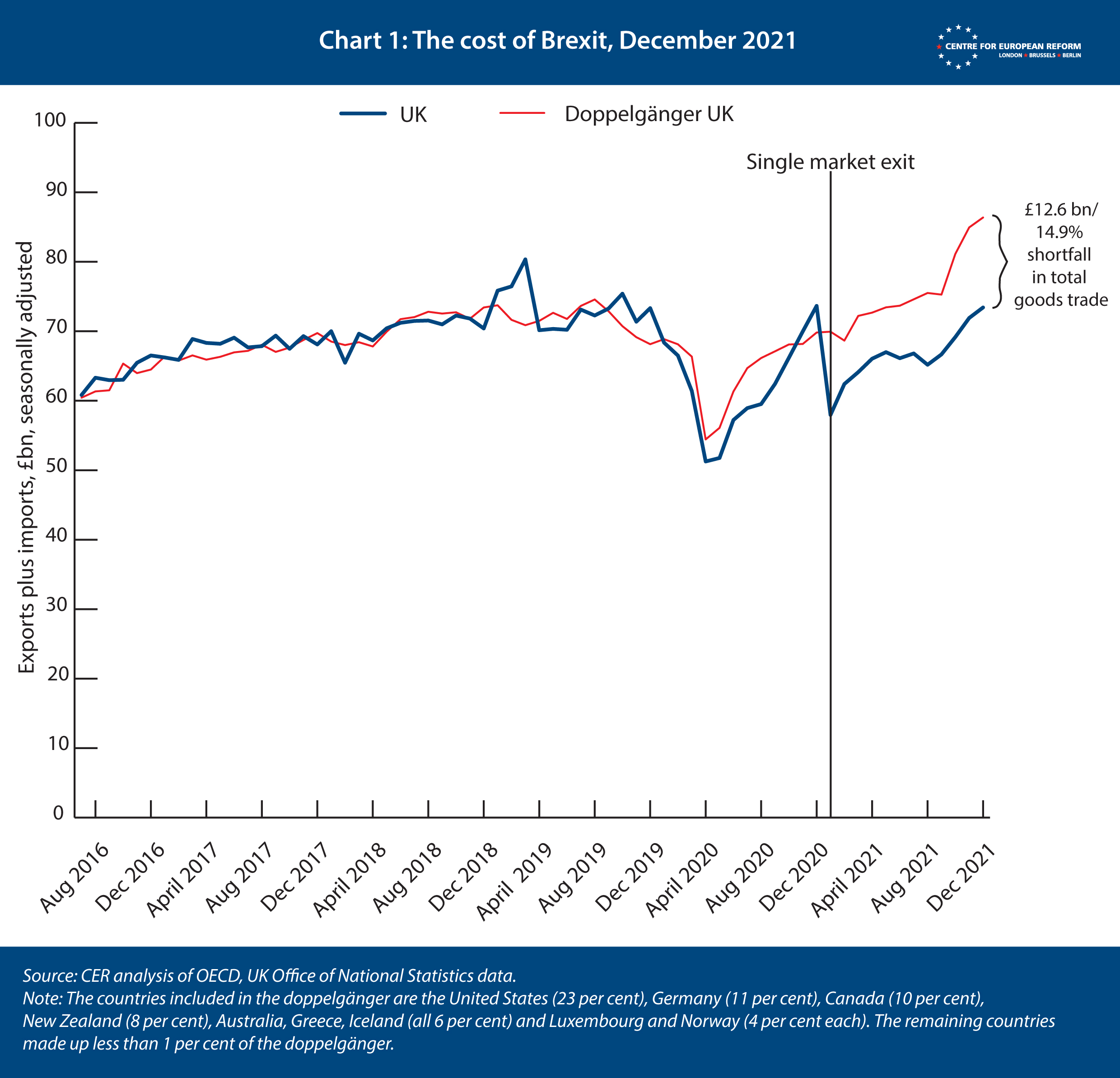

For many months, the CER’s cost of Brexit model has found that UK goods trade was between 11 and 16 per cent lower as a result of Britain’s exit from the single market and customs union. Using the data for December 2021, the model puts the trade loss at 14.9 per cent, or £12.9 billion for the month (Chart 1). That is a little lower than my last estimate, for October (15.7 per cent), because imports and exports grew more rapidly in December in the UK than in the doppelgänger UK.

The doppelgänger is a subset of countries selected from a larger group of 22 advanced economies by an algorithm. The algorithm finds the countries that, when combined, create a doppelgänger UK that has the smallest possible deviation from the real UK data from January 2009 to December 2019, before the pandemic struck. (The data includes goods trade, GDP growth, population, inflation, industrial production as a share of output, as well as some other measures. More information on the model, including Stata code and input data, is available here.)

Using the same method, we can study another contentious issue in the Brexit debate: trade experts have been puzzled by the fact that, on some measures, UK imports from the EU have suffered more than UK exports to the EU. Britain only enforced its border in a limited way until a year after the transition period ended, in January 2022, while the EU imposed controls on British exports immediately. The doppelgänger method, when applied to exports rather than total trade, shows that the UK’s goods export sector has been badly hit by leaving the EU. Both exports to the EU and the rest of the world appear to have been damaged by Britain’s withdrawal from the single market and customs union.

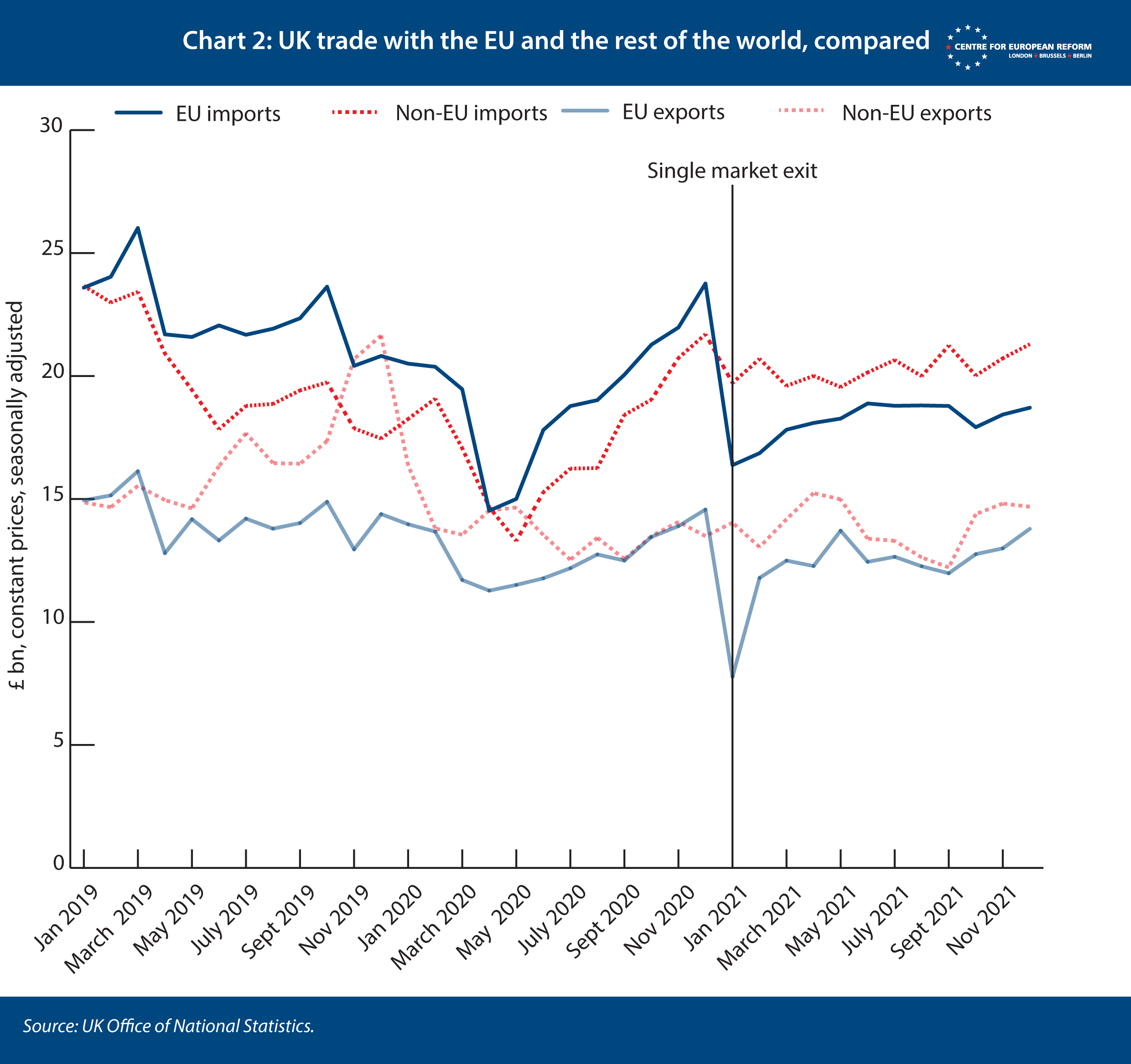

First, let us consider how analysts have considered Brexit’s impact on goods trade. The exports puzzle is explained by the way analysts are measuring the impact of single market exit. Many have compared UK trade with the EU to its trade with the rest of the world. Higher barriers with the EU should mean lower trade, while few new barriers to trade with the rest of the world have been imposed. On this measure, the difference between EU and non-EU trade serves as an estimate for how much trade has fallen.

Chart 2 shows that, UK exports to the rest of the world have been larger than exports to the EU since early 2019, and withdrawal from the single market does not appear to have reduced UK exports to the EU further. On the other hand, before leaving the single market, UK imports from the rest of the world were smaller than imports from the EU. The reverse has been the case after exit.

But comparing EU and non-EU trade has its problems. The UK, like many European countries, is an ‘intermediate’ producer of goods and services, with 65 per cent of its exports being used as inputs into the production process in the EU and other countries. It is therefore likely that barriers to trade with the EU are damaging UK exports to the rest of the world, which means that this method will underestimate the impact of Brexit on exports. UK exporters may be finding it harder to get the components they need from the EU, which might reduce sales both inside and outside the EU. And global manufacturing companies have switched the location of some of their plants to the EU, which would reduce UK exports generally if these companies use those plants to serve EU and non-EU markets.

The doppelgänger method overcomes this problem. The method compares UK exports to those of other advanced economies, which have taken part in an export boom since mid-2021 – one that Britain has missed out on.

Chart 3 shows that UK exports are 15.7 per cent smaller than those of an exports doppelgänger. There was a big export surge in the countries that make up the doppelgänger in 2020 and 2021 that the UK did not participate in, as economies reopened after the first wave of the pandemic, and demand for goods rose as consumer switched spending from services to goods. This synthetic UK was identified by the algorithm in exactly the same way as for total goods trade, except it found the countries that most closely matched the UK’s goods exports since January 2009, as well as the other predictors mentioned above.

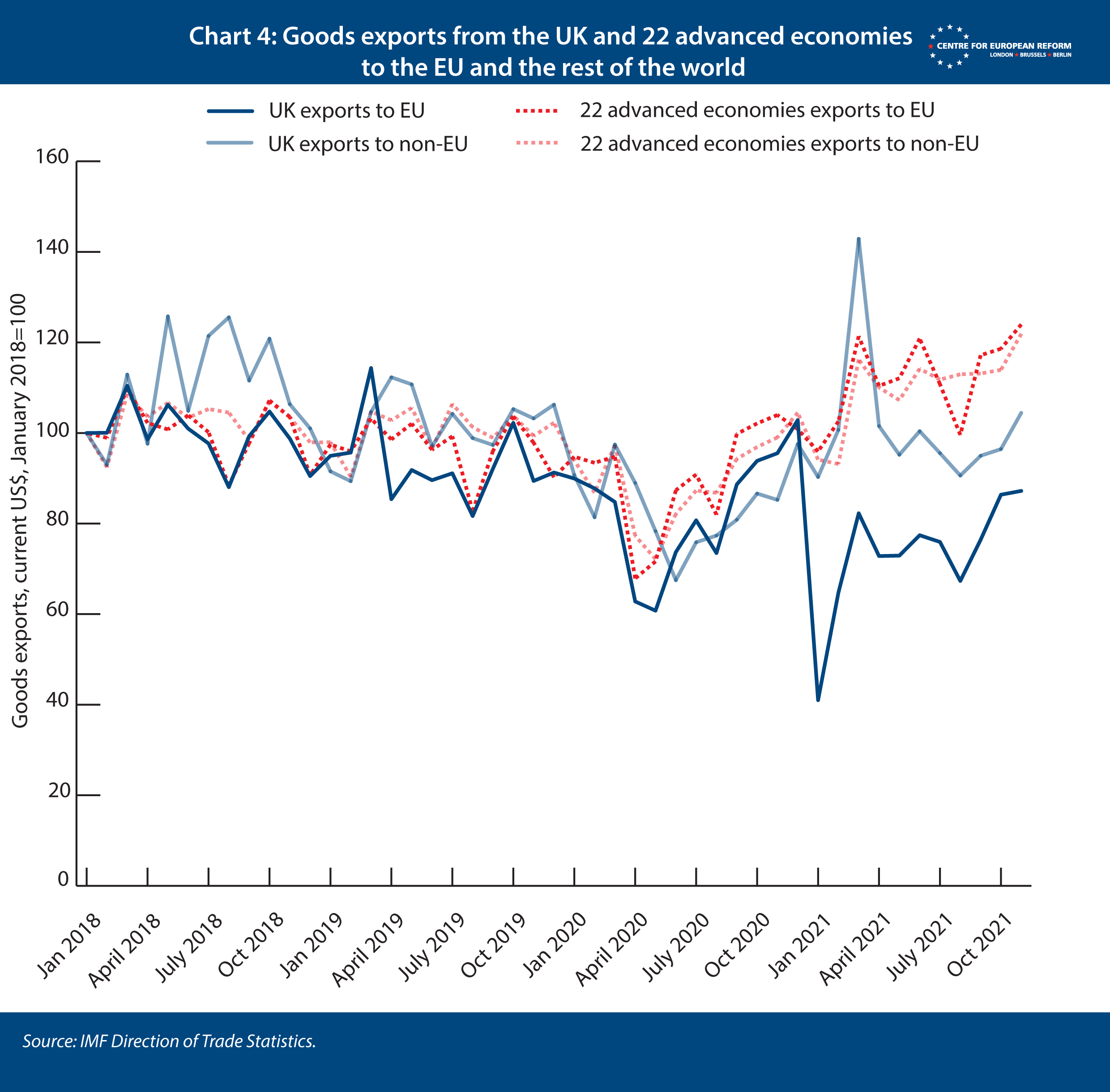

More evidence that Brexit has hit British exports to both the EU and the rest of the world is shown in Chart 4. On average, the exports of 22 advanced economies to both the EU and the rest of the world have grown rapidly since the depths of the first COVID-19 lockdown in May 2020. Meanwhile, UK exports to both the EU and non-EU countries have failed to keep pace.

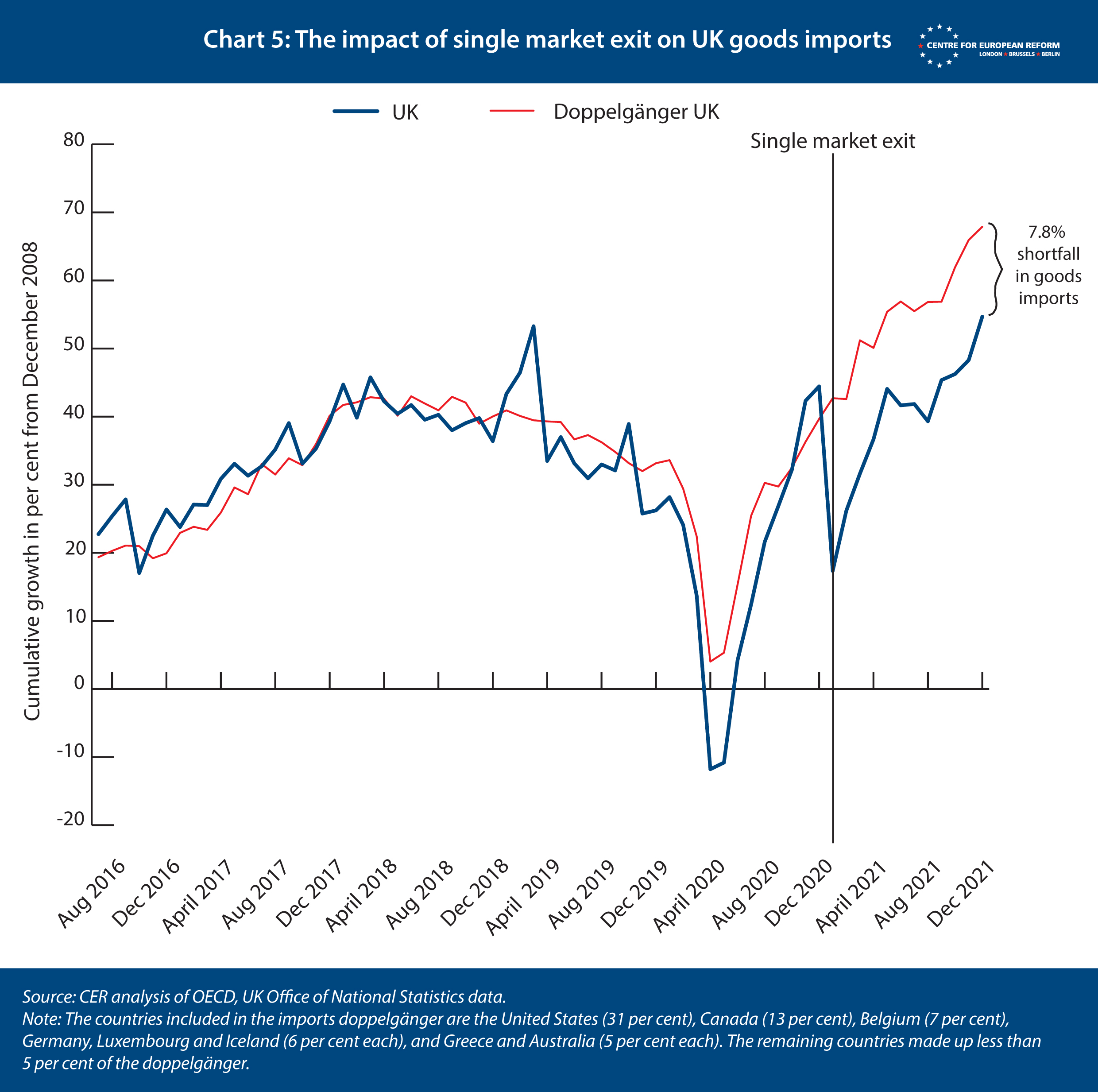

Turning to imports, Chart 5 shows a smaller, 7.8 per cent gap between Britain and the doppelgänger’s goods imports. Imports across advanced economies have surged even more than exports, especially since October 2021, when gas and oil prices spiked. (The countries that make up most of the doppelgänger are oil and gas importers, like the UK, and energy is included in the OECD monthly goods trade data that allows us to compare the UK to other advanced economies.) This evidence accords with the UK’s limited enforcement of its border in 2021.

The weakness of UK exports to both the rest of the world and the EU has important implications. Pro-Brexit politicians – and a few economists – have long argued that the UK might lose some trade with the EU but can make up for it by trading more with the rest of the world. They apparently did not realise that goods production has consolidated into three main regions – the EU, East Asia and North America – with components being traded within them multiple times across borders, with many final products being sold globally. Leaving the EU appears to have damaged the UK’s goods exporters serving markets both in the EU and beyond. ‘Global Britain’ remains little more than a slogan, at least in economic terms.

John Springford is deputy director of the Centre for European Reform.

Related content

The cost of Brexit: October 2021

Comments

If you take the example of medical face masks/respirators,prior to Covid all these products were imported, mainly from USA, China & smaller volumes from Europe with no UK production. Post Covid we now have 10 UK manufacturing plants with more than enough capacity to cover the UK market.

If the UK is really dependent on components etc. sourced from EU & barriers make it more difficult then more re-shoring will no doubt kick in.

There's no amount of "re-shoring" that can account for that diminishing of consumer market. And that is the bullet to the face that is Brexit. If we think the American market replaces the vast wealth European market, we are also deluded.

Add new comment